“This world keeps spinning / And with each new day / I can feel a change in everything”

“Well, it all keeps spinning, spinning ‘round and ‘round and upside down”

– Upside Down by Jack Johnson (2006)

In thinking about the investment markets over the last month and for the first quarter of 2025, this song, Upside Down by Jack Johnson, kept coming to mind. It is one of those songs that two people could draw inspiration from in very different ways. One could hear the light-hearted lyrics and melody and think that as the world keeps spinning it brings about a new day that offers a fresh opportunity to see the positive in life. Another listener can hear the same words and think what happened to the world they knew and why is it turning upside down. Both could be right, that is the beauty of the song.

Looking back at the first quarter of 2025, investors may be left in a similar state of mind, trying to interpret what happened to the investment markets that largely treated them well in 2023 and 2024. The positive interpretation of what occurred in the first quarter might focus on the beneficial cleansing of some of the excesses of the narrow US equity market and the rewards from remaining diversified with allocations to non-US equities and bonds. Even beaten down value investors are enjoying their time in the sun (hopefully it is not fleeting). While there may be some clouds, there will be sunshine ahead.

On the other side is a more negative interpretation that might focus on the sharp decline in growth stocks, the rising concerns about the trajectory of the US economy and a possible reignition of inflation due to the planned tariffs that could fuel a trade war. This view is reinforced by escalating geopolitical risks, rising political rhetoric across the US, and most significantly, uncertainty on how this will all play out in the coming months and years. Gray clouds could signal more storms ahead.

Historically, investment markets have recovered from periods of heightened volatility caused by shifts in economic conditions and policies. Excesses are washed out and investors focus on fundamentals and valuations. Markets and economies go through cycles of change, often brought about by unsustainable levels of optimism or pessimism. Typically, the investors who have the best outcomes are those who stay focused on their long-term goals while adapting their portfolios to the evolving market environment.

The song ends with this line: “is this how it’s supposed to be”. While not providing the clearest investment advice, at this moment this may describe how many investors are feeling as they look ahead to the spring quarter.

Here are some observations on what occurred across the public markets during March and Q1:

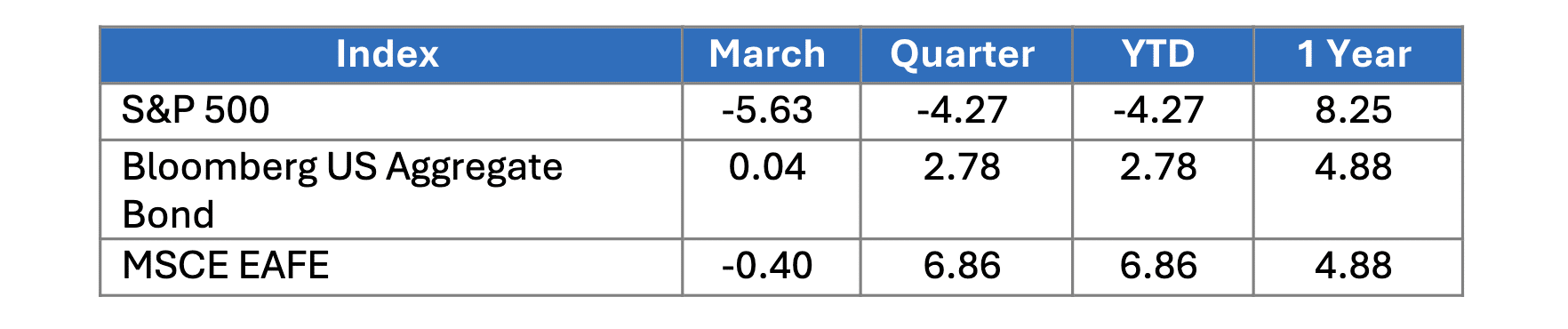

Broad Market Performance1

Domestic Equity2

- March was a difficult month for US stocks as the overhang of trade policy decisions and weakening consumer confidence contributed to sell-offs across most sectors.

- The negative results were most pronounced in large cap growth (the Mag 7 stocks were down 10%) and in small caps which have less flexibility to manage increased tariff costs.

International and Global Equities3

- Results were mixed for the month with value and small caps holding up better. For the quarter, non-US stocks outperformed US stocks by 11%, benefitting from the falling USDollar and increased fiscal spending.

- Emerging market stocks were positive for the month and quarter, led by China which rallied 15% in Q1 on additional economic stimulus.

Fixed Income Markets4

- Bond returns were mixed in March and positive in Q1 as interest rates declined and investors sought safety during the equity sell-off.

Specialty Markets5

- REITs declined along with equities in March yet retained much of their Q1 gains. Commodities rallied as gold and copper were up more than 20%.

Sectors6

- Energy and Utilities were the only positive sectors in March and the top performers for the quarter. Consumer Discretionary and IT were each down 13% in Q1.

Much like Jack Johnson’s Upside Down, the first quarter of 2025 left investors seeing the markets from different perspectives – some appreciating the benefits of diversification and resilience within their portfolios while others felt unsettled by sharp declines, economic uncertainty, and rising global tensions. Despite the turbulence, history reminds us that markets tend to recover as investors refocus on fundamentals.

As always, staying grounded in long-term goals is key. If you have questions or want to discuss how this evolving landscape may impact your plan, please do not hesitate to reach out to your advisor—we are here to help.

1-6 All data supplied by Morningstar.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from HUB International or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professionals, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

HUB Retirement and Private Wealth employees are Registered Representatives of and offer Securities and Advisory services through various Broker Dealers and Registered Investment Advisers, which may or may not be affiliated with HUB International. Insurance services are offered through HUB International, an affiliate.